By Kai Ioh and KE TEAM Hawaii

Kai Ioh is a luxury real estate advisor based in Kona, Hawai‘i, specializing in second home, resort, and ultra-high-net-worth markets across the Big Island.

Key Takeaways

- National housing inventory has begun declining after nearly four years of growth.

- More homes are selling across the United States, while fewer new sellers are entering the market.

- Local markets are increasingly moving in different directions, making national averages less useful by themselves.

- Inventory in many Big Island luxury and resort communities remains above last year’s levels. But market conditions differ by area and price range.

- Buyers continue to have opportunities, while sellers must focus on pricing, presentation, and market positioning.

National Housing Inventory Is Starting to Shrink

After nearly four years of steadily rising housing inventory across the United States, something interesting has happened.

The trend has quietly shifted.

For the first time in several years, there are now slightly fewer homes for sale nationally than there were a year ago. While the change is modest, inventory remains one of the most important drivers of real estate markets.

Over the past several years, buyers benefited from steadily increasing choices as more homes came onto the market. Today, that trend appears to be reversing.

According to Mike Simonsen, Chief Market Analyst at Compass, total U.S. inventory recently fell below one million homes and slipped below year-ago levels despite expectations that supply would continue growing throughout 2026.

In the context of Hawai‘i, this matters because many Big Island buyers originate from mainland markets where inventory trends often influence confidence, equity growth, and purchasing decisions.

Why Is Inventory Declining?

Several recent indicators point to a gradual shift in market direction:

- National inventory has fallen below last year’s levels.

- New listings are averaging approximately 96,000 homes per week, only modestly above last year.

- Pending sales during May increased approximately 6% compared to the prior year.

- Price reductions remain elevated at roughly 37% of listings but are no longer accelerating.

- The median national asking price is approximately $442,000, about 2% below last year.

The underlying story is relatively simple.

More homes are selling, but not enough new sellers are entering the market to replace them.

As a result, inventory is slowly shrinking.

This is not a dramatic shortage of supply. However, it does represent an important change in direction after several years of inventory expansion.

Why National Housing Data Is Becoming Less Useful

One of the most interesting observations highlighted by recent Inman reporting is that national inventory numbers are becoming less meaningful by themselves.

On the surface, the national housing market appears relatively balanced.

Underneath, however, local markets are telling very different stories.

Some Markets Remain Supply Constrained

Several major metropolitan areas continue facing inventory shortages.

Markets such as New York and Chicago have experienced limited supply and continued price appreciation, with home values rising in many neighborhoods despite higher mortgage rates.

Some Markets Are Working Through Excess Inventory

Several Florida markets that experienced significant inventory growth over the past few years are now beginning to see supply decline as excess listings are sold or withdrawn.

In these areas, inventory remains elevated compared to pre-pandemic levels, but conditions are gradually rebalancing.

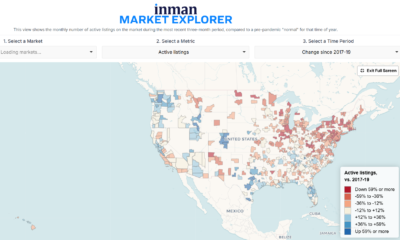

INMAN National Inventory Level Comparison (2026 vs. Pre-COVID)

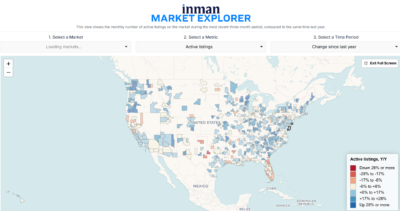

INMAN National Inventory Comparison (Year-over-Year change)

Some Markets Continue Adding Inventory

Seattle remains an example of a market where inventory growth continues.

New listings have remained above year-ago levels, creating additional opportunities for buyers.

The result is a national housing market that looks increasingly fragmented.

Local conditions matter far more than broad national averages.

Why This Matters for Hawai‘i

For many Big Island property owners, mainland housing markets remain important.

A significant percentage of buyers in Kona and along the Kohala Coast come from:

- Seattle

- Los Angeles

- Orange County

- The San Francisco Bay Area

- San Diego

- Utah

These markets continue to generate demand for:

- Second homes

- Resort residences

- Retirement properties

- Luxury lifestyle purchases

When inventory tightens in these feeder markets, homeowners often gain equity and confidence, which can eventually support demand for second homes and resort properties in Hawai‘i.

That said, not all feeder markets are moving in the same direction.

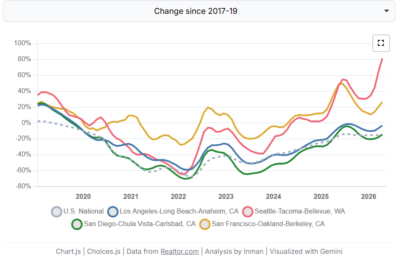

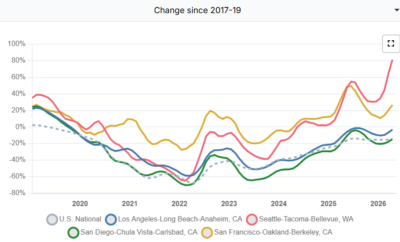

Recent Inman data illustrate how differently inventory levels are behaving across major feeder markets, including Los Angeles, San Francisco, San Diego, and Seattle. Seattle and San Francisco, in particular, have experienced greater volatility than Los Angeles and San Diego in recent years.

INMAN Inventory Level Comparison- LA, SF, SEATTLE and SD (2026 vs. Pre-COVID)

INMAN Inventory Level Comparison- LA, SF, SEATTLE and SD (2026 YoY comparison)

However, it is important not to oversimplify the discussion. Real estate markets are increasingly local, and each feeder market comprises multiple submarkets with distinct dynamics.

San Francisco is a good example. While some Bay Area neighborhoods continue adjusting to post-pandemic shifts, portions of downtown San Francisco are benefiting from renewed demand tied to the ongoing AI boom. Employment growth, office leasing activity, venture capital investment, and housing demand are not being distributed evenly throughout the region.

The same pattern exists in Southern California, Seattle, and other major feeder markets. Broad inventory statistics provide useful context, but understanding what is happening beneath the surface often matters more than the headline number itself.

Over time, tighter inventory in the feeder markets will support demand for Hawai‘i real estate.

Stock market performance also remains a significant factor.

Unlike many primary-home purchases, luxury and resort transactions are frequently influenced by investment portfolio performance and overall household wealth.

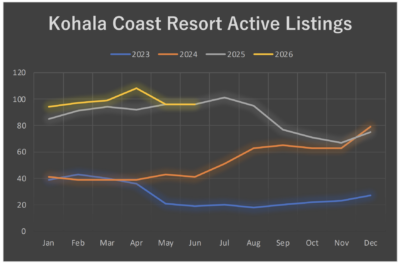

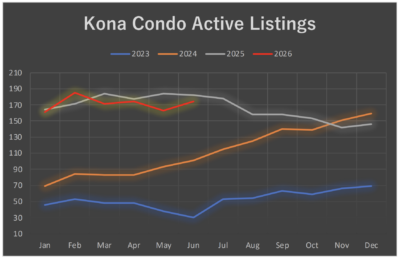

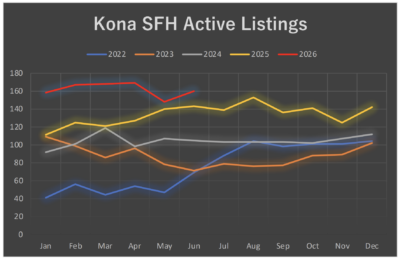

Is the Big Island Following the Same Trend?

Not exactly.

While the Kona condo has fewer inventory, the Kona SFH has more inventory available than they did one year ago. The resort condo market inventory has decreased to last year level.

For buyers, that creates opportunities.

They can compare properties more carefully, conduct additional due diligence, and often negotiate more effectively than they could several years ago.

The environment is more balanced than it was during the peak pandemic period.

What Does This Mean for Big Island Sellers?

The market has become increasingly selective.

The days of simply placing a property on the market and expecting multiple offers are largely behind us.

Today’s buyers are evaluating properties carefully and comparing multiple options.

As a result, successful sellers are focusing on three areas.

Accurate Pricing

Properties priced appropriately continue attracting attention.

Listings that begin too aggressively often require price adjustments later.

Strong Presentation

Professional photography, thoughtful preparation, maintenance, and staging remain important competitive advantages.

Buyers notice details, particularly in the luxury market.

Realistic Expectations

Many markets remain healthy, but conditions today differ from those seen between 2020 and 2022.

Preparation, patience, and strategy have become increasingly important.

The Mortgage Rate Wild Card

The biggest variable remains interest rates. Mortgage rates have recently moved back into the upper six percent range, which continues to affect affordability and buyer confidence.

At the same time, strong stock market performance continues supporting many affluent buyers.

The market is currently balancing between these two forces:

- Higher borrowing costs

- Strong investment portfolios

If rates remain elevated, sales activity could moderate.

If rates stabilize or move lower, inventory could tighten further and place additional upward pressure on prices.

As Mike Simonsen has noted in recent housing inventory analysis, today’s market appears less driven by a surge in demand and more by a gradual decline in available supply.

That distinction matters.

What Should Big Island Buyers and Sellers Watch?

The national housing market appears to be entering a new phase.

Inventory is no longer expanding as it has over the past several years. Instead, supply is beginning to contract modestly while sales activity improves.

That does not necessarily mean prices are about to surge.

In many markets, prices remain relatively stable. What it does suggest is that momentum may be shifting.

For buyers and sellers on the Big Island of Hawai‘i, the most important lesson remains unchanged:

Real estate is local.

Conditions in Seattle, California, Florida, New York, and Hawai‘i can look very different from one another.

National headlines provide useful context, but local inventory levels, buyer behavior, and pricing trends ultimately drive decisions here in Kona and along the Kohala Coast.

Understanding both the national picture and the realities of the local market helps buyers and sellers make better-informed decisions.

Sources and Market Data

This article incorporates national housing inventory analysis from Mike Simonsen, Chief Market Analyst at Compass, as well as regional housing market reporting published by Inman News during May and June 2026, and local MLS data.

Frequently Asked Questions

Is national housing inventory declining in 2026?

Yes. National housing inventory recently fell below year-ago levels after nearly four years of steady growth.

Why is inventory shrinking?

More homes are selling while fewer new sellers are entering the market, causing available inventory to gradually decline.

Does lower inventory automatically lead to higher prices?

No. Prices are influenced by inventory, mortgage rates, affordability, employment conditions, and buyer demand.

Is the Big Island experiencing the same inventory decline?

Not in many luxury and resort communities. Several Big Island markets continue to have more inventory than they did a year ago.

Why do mainland markets affect Hawai‘i real estate?

Many Big Island buyers come from mainland markets. Housing equity, market confidence, and investment performance in those areas often influence purchasing decisions in Hawai‘i.

Are buyers still able to negotiate on the Big Island?

In many market segments, yes. Buyers generally have more choices today than during the highly competitive pandemic-era market.

What should sellers focus on today?

Accurate pricing, strong presentation, and realistic expectations remain essential.

How do mortgage rates affect luxury real estate?

Luxury buyers are often less rate-sensitive than traditional buyers, but financing costs still influence overall market activity and buyer confidence.

Is this currently a buyer’s market or a seller’s market?

The answer depends on location, price range, and property type. Many Big Island luxury segments are currently more balanced than they were several years ago.

What is the biggest misconception about national housing trends?

Many people assume national statistics apply equally everywhere. In reality, local housing markets often move in very different directions.